Rhode Island employers and families are once again confronting substantial proposed increases in commercial health insurance premiums. For 2027, insurers have requested average increases of 20.1% for the Individual market, 8.7% for the Small Group market, and 15.5% for the Large Group market.

These requests come immediately after the Office of the Health Insurance Commissioner approved 2026 increases of approximately 21.0% for Individual plans, 17.6% for Small Group plans, and 19.3% for Large Group plans. While OHIC will now review the 2027 filings and historically has approved roughly 80% of requested increases, employers should prepare for the possibility of a second consecutive year of unusually large premium increases.

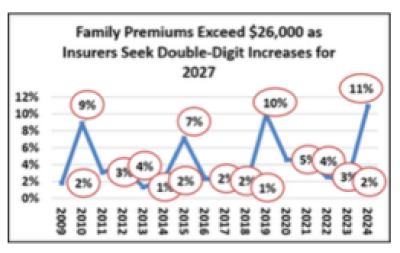

From Record Premiums to Consecutive Years of Large Increases

The accompanying chart shows where Rhode Island stood before the current rate review cycle began. By 2024, the average family premium in Rhode Island had climbed to nearly $26,000, almost double the level recorded in 2008.

For many employers and families, figure alone is alarming. But the chart does not yet reflect what happened next.

Following the 2024 survey year, Rhode Islanders experienced approved 2026 premium increases ranging from roughly 18% to 21%, depending on market segment. Now insurers are requesting another round of substantial increases for 2027. If OHIC follows its recent pattern and approves most of the requested increases, Rhode Island will have experienced two consecutive years of premium growth that far exceeds general inflation.

Viewed in this context, the concern is not simply the size of any single year's increase. The concern is that already-record premiums are being followed by successive years of unusually large increases. What was already becoming difficult for employers and families to afford may soon become even more challenging.

Rhode Island's Affordability Challenge

Rhode Island often points to having the lowest family premiums in New England. While that is true, it does not tell the entire story. For many years, Rhode Island's family premiums, deductibles, and out-of-pocket maximums have remained near the national average.

The challenge is that the national average itself has become increasingly unaffordable. Being average in a system that is becoming less affordable each year is not a long-term success. Rhode Island should aspire to be below the national average and become a state where affordable health coverage is viewed as a competitive advantage for attracting and retaining businesses.

What Continues to Drive Costs?

Data from both national and Rhode Island sources consistently show that hospital spending remains the largest component of commercial premiums, accounting for nearly half of every premium dollar. Hospital outpatient spending in particular has grown substantially over the past decade.

Prescription drugs, provider consolidation, administrative complexity, state and federal policy decisions, and cost shifting from public programs also contribute to upward pressure on premiums. Yet despite years of discussion about affordability, the fundamental drivers of health care costs remain largely unchanged.

The Need for a Different Approach

The recurring cycle of double-digit premium increases raises an important question: how many more years can employers and families continue to absorb these costs?

Rhode Island has begun exploring reforms such as the AHEAD model and other payment initiatives designed to improve efficiency and better align incentives across the health care system. These efforts deserve attention and support. However, meaningful progress will require a shared commitment among providers, insurers, employers, and state leaders to address the underlying drivers of cost growth rather than simply financing them through higher premiums.

The 2027 filings serve as another reminder that the current trajectory is not sustainable. Whether the final approved increases are somewhat lower than requested or not, the trend is clear. Without meaningful change, Rhode Island employers and families should expect to face the same affordability challenges year after year.